As widely expected, the Reserve Bank of Australia has left the official cash rate at an “accommodative” 2.5 per cent citing “on present indications, the most prudent course is likely to be a period of stability in interest rates.”

This now has many calling a bottom to the interest rate cycle.

The statement on today’s monetary policy decision reports, “The demand for labour has remained weak and, as a result, the rate of unemployment has continued to edge higher. Growth in wages has declined noticeably.”

“Looking ahead, the Bank expects growth to remain below trend for a time yet and unemployment to rise further before it peaks.”

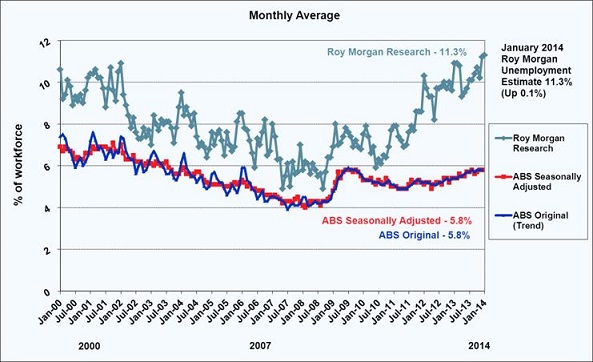

Roy Morgan today released unemployment figures for January 2014 showing unemployment is now 11.3 per cent, the highest result since January 1995. 1.44 million Australians are now out of work and another 1.105 million are under-employed. Together, this makes up 20 per cent of the workforce.

Since departing from ABS index in 2010, there is a distinct upward trend in the Roy Morgan unemployment figures with no signs of abating.

Yesterday, MacroBusiness published insights from Saul Eslake (‘Eslake: Unemployment much higher than it looks‘) on expectations of continued deteriorating unemployment. Eslake noted, “The RBA has never raised rates while the unemployment rate is rising; indeed, it tends to keep lowering them.

“Further, we argue that given the majority of the decline in participation is of prime working age people, rather than retirees, and therefore it is akin to uncounted unemployment. From this we conclude that the actual unemployment rate is significantly worse than official [ABS] figures suggest. As we continually stress, if the participation rate had remained at the 2009-11 average then the unemployment rate would be 7.1%. The increase in this adjusted unemployment rate has accelerated markedly over the second half of 2013. And it is this that leads us to believe that the RBA may be getting behind the curve on labour market weakness.”

His analysis includes a graph, published in the Macrobusiness article overlaying the official unemployment rate, cash rate and a “participation adjusted” unemployment rate, clearly highlighting his claims the RBA is falling behind the curve on unemployment.

» Statement by Glenn Stevens, Governor: Monetary Policy Decision – Reserve Bank of Australia, 4th February 2014.

» Eslake: Unemployment much higher than it looks – Macrobusiness, 3th February 2014.

Interest set at a record low for some time now.

Retail and services sector are completely unresponsive (not my words, but I believe it was Adele Furgeson).

The only things rising in price are:

Government fees/charges/fines

House prices

Large business charges ie. insurance company premiums

Small business is in a blood bath.

General retail is in a blood bath.

The #1 goal of RBA (or any central bank for that matter) is to control inflation.

I just can not see inflation picking up any time soon. Therefore despite the RBA’s cryptic statements interest is far more likely to lower.

In fact they can’t raise rates, we are now where the USA was in 2005. They had stupidly low rates from the Dot com bust & 9/11 which bred their housing bubble. We have now had low rates for 5 years also, which has bred the super bubble.

Once rates rise in Australia that’s when the real party will begin. I had stupidly assumed that the crowd (ie. property purchasers) would see the error of their ways and slow down on pushing prices up. But I have since learn’t that human greed will ensure that even as mortgagee auction rates become parabolic people will still be paying WAAAAYYYYY too much for property.

Only once panic hits the market (induced by interest repayments that simply CANNOT be met) will the tide go out so we can see who is swimming naked.

So, we all know unemployment is way up. Every second person I talk to has family who can’t find SUSTAINABLE work.

Just wake me when interest rates start their ascension. I’m not missing that party. Just make sure you have a VIP ticket.

its easy to see Australia is fast becoming the next Ireland, costly to do business and soaring labour costs, this country is loosing its manufacturing industry, the biggest problem is that property investors should be capped on the amount of property they can buy, greedy investors keep hard working aussies off the property ladder, its these parasites of investors have created the bubble in Australia, I cant wait for the day when everything goes tits up and the investors are stuck with all their properties and banks hounding them for the mortgage repayments, its going to be very interesting to see what happens in the near future.

No wonder the Federal budget is collapsing with this level of unemployment. It explains why Joe Hockey wants to soften us up before May so the shock is not as great.

Because of NG, if interest rates start to rise Property Investors will simply claim more tax off their income; in other words the tax payer(you and me) will pick up the bill.

If the Property Investor is not Negatively Geared they will simply put the rent up and the tenant will pick up the bill.

Just when you thought things couldn’t get any more ridiculous.

http://www.macrobusiness.com.au/2014/02/foreigners-cashing-in-on-nsw-new-home-grant/

How many single parents who borrowed or took over low-doc loans are there relying on Centrelink and child-supp payments alone? Or with part-time only jobs? I know of someone who survives on a combination of the three with three teen money vacuums in tow. If jobs really slide, this will get very messy through the generations….

Little birdie just told me Govt is going to loosen up the chinese investment tap even more. They are going to drive prices sky high because its great for their portfolio and everyone gets happy when house prices rise. Sure the average wage vs price is 10x+ now but hey… the majority of voters are 30+ and lovvvvvve rising house prices. It makes them feel rich.

Ford’s at it too.

http://www.heraldsun.com.au/news/victoria/ford-workers-face-300-job-cuts-at-broadmeadows-and-geelong-plants/story-fni0fit3-1226819477821

Hushtastic – Nothing of this magnitude stops simply because of common sense. As someone stated elsewhere, the only way is when things become IMPOSSIBLE. Rising repossesions. Rising unemployment. Rising number of people on welfare etc etc.

Honestly, no one gives a flying F… and why should they? Coz it’s right? LOL… yeah…

Yep, the 11.3 percent only covers citizens currently unemployed. It doesn’t count all the Ford/Holden and Toyota jobs yet to go, nor all the jobs in the component suppliers. Lot more job losses in the pipeline.

Hushtastic-

you had better get in quick and get a couple of properties then. Never been a better time to buy with your reasoning and when you get to 10 times income you can get yourself a new Audi like so many others.

Besides, everybody known that it is Chinese buyers and Investors that underpin the market and not FHB.

Good Luck

…

I just had to deal with one of my employees quit.

She was just crying and crying about how she loves the work but knows we cant pay her more and she cant afford a house so she’s going to work on the mines as a cleaner as opposed to being a social worker looking after disabled children. She doesn’t want to move to a country with cheaper housing because her friends and family are here.

Depressing.

Shes smart and works hard. Shame to lose the talent because she actually cares.

Oh shes 25 and rents because of a bad family life so she was committing herself to helping other families.

This is a ton of social issues ‘symptoms’ stemming from one disease which can be cured with 1 law.

I’d pay her more but our budget got cut last year and I’d have to fire someone.

Don’t worry guys before you know it our government will be dropping those freshly printed $50 bills from the sky and all the party voters will be happy again.

I think that we have reached a permanent plateau of house prices. The property market has decoupled from unemployment and rent, thanks largely to our asian friends who are more than willing to buy anything they can get their hands on …. and let it sit empty.

There’s a 5k grant from the NSW Govt for overseas buyers just to seal the deal.

I’d have to agree with Macrobusiness who have described our government backed property market as a ‘permabubble’.

And it will only get worse (or better according to the property lobby and msm) as there is no one to vote for on this issue.

‘They’ have won.

You may be right average_bloke.

They don’t seem to care that they are forcing our greatest young talent overseas and bringing in cheap foreign labour to drive down wages. We are so uncompetitive now it doesn’t seem to matter to them.

Hide the real unemployment figures and hope people keep coming here making sure they have plenty of money in their pockets to plug the holes.

Mind you, if the world actually gets wind of what is happening here jobs wise and other temporary workers here ( 457s, working holiday makers, students and Kiwis) start to find out the lucky country is not what it seems the immigration flows might start to mirror that after the GFC.

Maybe the government and the banks will start shipping money to China to keep their boat afloat just so ours doesn’t spring any more leaks.

Welcome to the new normal.

http://www.heraldsun.com.au/realestate/ing-first-homes-buyers-increasingly-spending-a-million-dollars/story-fnhytr0m-1226820981579

How long can this madness go on for?,$1million just for an a average home?

The only first time homeowners, or anybody else who can afford to spend $1 million on an average home, would definitely not be earning “average incomes”. Even if you had a deposit of say $300K (and the vast majority of people don’t have that kind of money), that means you have to borrow well over $700K to cover the balance and the extra costs ie. stamp duty, legal fees, real estate agent commissions etc.

The only people who could afford such massive mortgages are successful self employed business people, CEOs on salaries well over $500K, or someone like a successful barrister earning serious money. But god help you should you or your partner lose your job/or your business goes bad, and given the fact the Australian economy is going pair shaped fast, the amount of mortgage stress must be going through the roof.

Master Yoda-

Articles like this, designed purely to encourage first time buyers to compete with investors would be funny if not for the terrible harm they will cause.

With first time buyers at record lows and the MSM pushing large mortgages on the naive surely means we will see an end to this madness within a couple of years.

Million Dollar Mortgage Slaves:

http://www.adelaidenow.com.au/realestate/million-dollar-mortgage-slaves/story-fni0c830-1226820840059

@ Glen

Love the line about ‘don’t worry as the price of the house will have gone up to cover it’s cost over 30 years.

ROFL: Someone should tell her that FIAT currencies have an average life span of 40 years……..

This house of cards gets scarier by the day:

On the one hand sometimes even I doubt the fact I stayed out of the market: But clearly the local economy can not last forever in it’s current position.

Then when you factor in the global economy, and how close it came to collapse in 2007-2009….and how things are actually far worse now than then, it’s only a matter of time before an enormous economic disaster strikes.

A combination of sound politics (despite how we crow how bad our politicians are, we have a very, very stable society) and a smooth progression from gold backed to gold reserves to FIAT currency has seen people be willing to take on crazy amounts of debt in the belief that cos it’s been ok for the last x number of years, the next x number will be the same.

Not so! I honestly believe the kids who are now in school will be like our great grand parents who saw the depression and lived modestly, often accumulating astonishing wealth: Compare this to our current baby boomers and SKI’s.

Then compare gen x & gen y….they will have no legacy: Actually they will: They have built the most profitable banking system ever known (for now)

The alternative to this madness is to rent, save the (as we know rather substantial) difference, and buy a place outright either in Australia or somewhere else later in life should you choose. At least you have that option, but if house prices take a protracted, decades-long slide (like in Japan), you and your children’s futures are going to look pretty bleak.

No government in league with the banks should ever be allowed to interfere in housing markets, that’s the lesson to take home here.

@ Chockolate

The real lesson is that central and privatised banks are more dangerous than standing armies…….

The 3rd president of the USA, Thomas Jefferson (1743 – 1826) once said “I believe that banking institutions are more dangerous to our liberties than standing armies. If the American people ever allow private banks to control the issue of their currency, first by inflation, then by deflation, the banks and corporations that will grow up around [the banks] will deprive the people of all property until their children wake-up homeless on the continent their fathers conquered. The issuing power should be taken from the banks and restored to the people, to whom it properly belongs.”

Ah yes, but that would be communism, wouldn’t it! Just look at what’s happened to every nation that’s nationalised anything in the past century – war, assassinations, embargoes…

In Australia here we missed out on a lot of that, but now we aren’t looking so immune.

http://mobile.abc.net.au/news/2010-11-17/people-who-lend-cars-for-weddings-may-face-jail/2340218

SA has found a way to make money

I just realised how old that article is! Goes to show though hey?

http://www.abc.net.au/news/2014-02-11/investors-at-decade-high-drive-growth-in-home-lending/5252294

I suppose when RP Data personal themselves start suggesting we are now in danger territory, and the possibility of ‘closed door’ meetings amongst the banks, suggest once more just how close we are sailing to the wind.

Hi Chockolate,

Jefferson was talking about real money Gold silver.

As opposed to paper currency created by a private bank like the us federal reserve

not communism.

These banks and this paper is unconstitutional even in Australia

short story

http://www.silverseek.com/article/silver-saga-7861

prepper

Here we go again!

http://www.news.com.au/finance/real-estate/is-it-cheaper-to-rent-or-buy/story-fncq3era-1226824506086

Surprise surprise, they don’t appear to have factored in any of the maintenance costs, insurance, rates, depreciation…

………

prepper

I imagine we have all heard the news that Toyota has announced that its pulling up stumps in 2017, thus nailing the final coffin in the Australian Car industry.

Virtually every week, some company is either closing down or being outsourced to some low cost country eg.China,Thailand,India etc, resulting in thousands of Aussie jobs lost, and more people joining the ever lengthening dole queues.

What industries does Australia have left?, mining and of course the Government/bank Ponzi scheme also know as the property bubble and tons of household debt. I don’t know, but I hold grave fears about where the Aussie economy is headed.

Chockolate,

Even if it’s the same… I don’t really believe the house/unit (especially unit) will be worth even $1mil at the end. You will also have difficulty selling it by the time we’re done with this show.

Now correct me if I’m wrong, but isn’t this how it went down elsewhere?

Record property prices, cheap credit, easy loans, “always goes up” , then the jobs start shedding, confidence plummets then the SHTF.

‘No one coulda’ seen this comin’…’. We’ll here that an awful lot soon enough.

“Australia readies more than $100 billion in asset sales”

http://www.marketwatch.com/story/australia-readies-more-than-100-billion-in-asset-sales-2014-02-12

@Ripa – You are right, you can lower interest rates to cushion the blow of extremely high household debt levels, but there is nothing you can do for when unemployment rolls through. People are simply unable to service their horrendous mortgages or pay high rents.

This is just the tip of the ice burg for unemployment. These figures are from January (Like the ABS that were released yesterday showing unemployment is the worst in 10 years) and don’t include the shutdown of the Automotive Industry (Holden, Ford, Toyota and the component suppliers) or other job losses that have been announced, but are let to occur – orderly shutdowns.

@Yusuf,

“We are going to free up the capacity to get on with the job of building things,” Mr. Hockey told The Wall Street Journal

Is this just selling off stuff we’ve already paid for via taxes? That’s not growth, and we know how this ends when the same services come back to us with government guaranteed profit padded into it at every step. Privatisation always ends up that way.

In my opinion, if that happened, you will see more reshuffling. More job losses or not, I can’t say but I think it will be “harder” than currently is.

On the flip side, I can sense the rationale of such choice. It will stir more competition in used to be regulated industries.

Then again, I will be asking “Why did you block the takeover of ASX by SGX last time in the name of protecting National interest? Why did AWB deal fall to go through? That is a puzzle for me.

Ups… Graincorp Lrd

We live in a Global community now. Economics is like the ocean that connects our community together.

The major economy’s are not and have not been in recovery. Since the GFC started in rehypothecated sub prime mortgages in the us. We now have another wave of GFC on its way here.

http://www.silverdoctors.com/20-signs-that-the-global-economic-crisis-is-starting-to-catch-fire/

prepper

Alcoa – Point Henry closure

http://www.smh.com.au/business/alcoa-announces-closure-of-point-henry-aluminium-smelter-20140218-32wzq.html

Sorry to be bearer of more bad news, but Alcoa has announced that 1,000 jobs will be lost as the result of their decision to close their plants in Geelong and Yennora.

I guess for the older workers nearing retirement age who have already paid their mortgages off in full, the redundancy package they will get will be a nice bonus. However, what about the younger workers with massive mortgages hanging over their heads?

One thing for sure, the city of Geelong is being hit hard with the closure of Ford, and now Alcoa.I think former prime minister Paul Keating was right when he said Australia is becoming a “banana republic”, I think we are already there now because the Aussie economy is turning to custard real fast.

One main contributor in all of this: Cost of labour.

Sure, sure, high dollar, un-fair free trade agreements, environmental considerations, stable government & taxation, distance etc. etc. all play a part.

Remember through any economic turmoil ahead, that it will only turn to custard for those who don’t prepare for it…..or signed on to economic slavery to a bank loan.